Brand new summer drop

Hamburger

Comprehensive Study Materials for Students of All Courses

Home

All Products

MYR

Chevron Bottom

USD

EUR

CAD

GBP

AUD

NZD

SEK

NOK

DKK

PLN

INR

JPY

MYR

SGD

MXN

BRL

CHF

Cart

Close

All Products

Big Data Analytics with Apache Spark

RM 40.57

An Introduction to Scala for Spark programming

RM 40.57

Big Data Analytics - Information retrieval

RM 40.57

BDA Lc03 Basic algorithm design- Big Data Analytics

RM 40.57

BDA Lc02 Developing a MapReduce application

RM 40.57

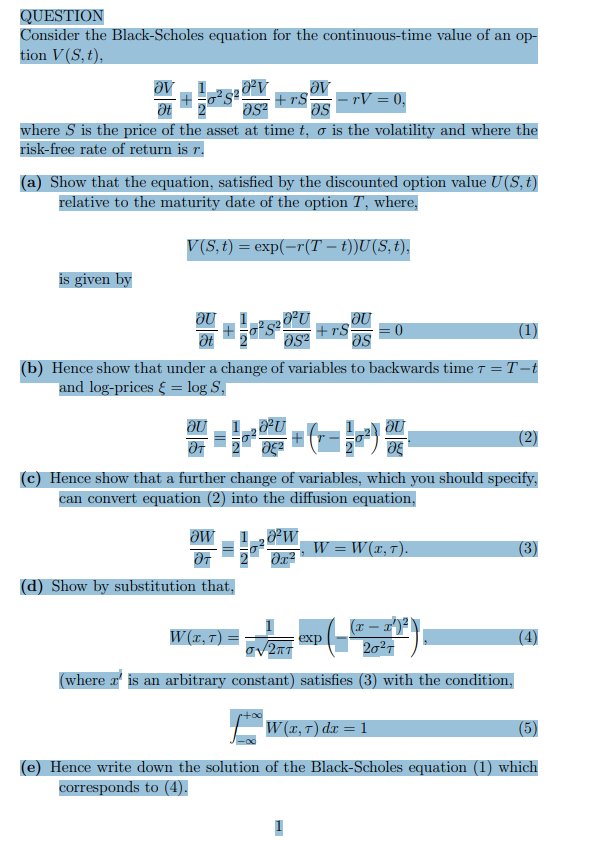

TD - Using the Black-Scholes equation for a continuous-time value of an option

RM 40.57

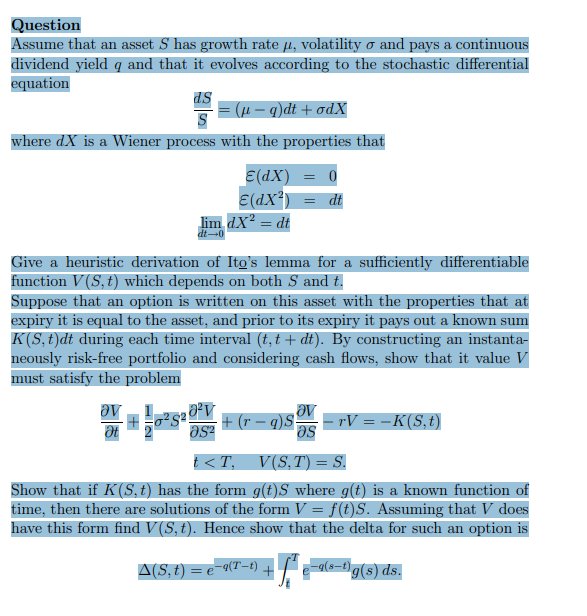

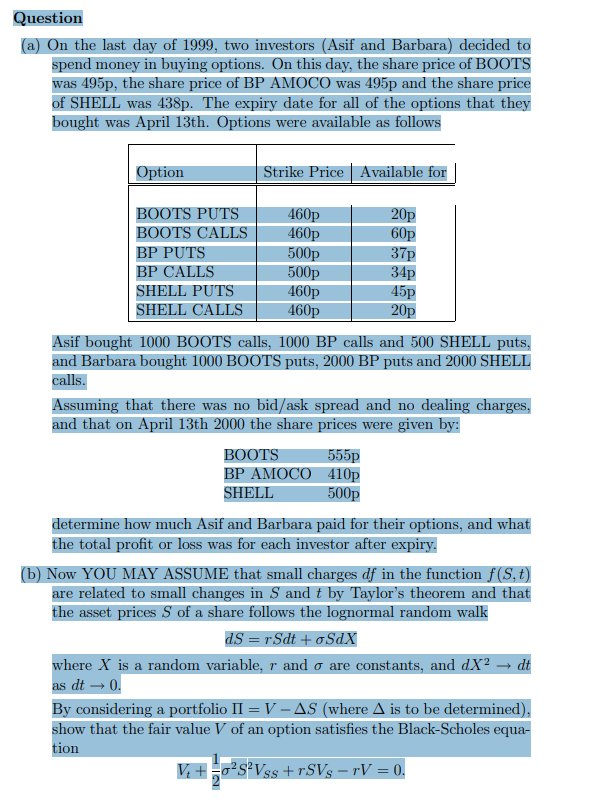

TD - Stochastic differential equations and instantaneously risk-free portfolios

RM 40.57

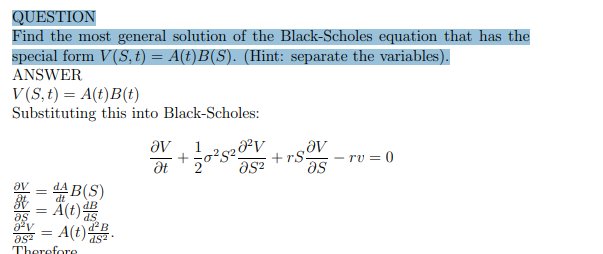

TD - Solutions of the Black-Scholes equation

RM 20.29

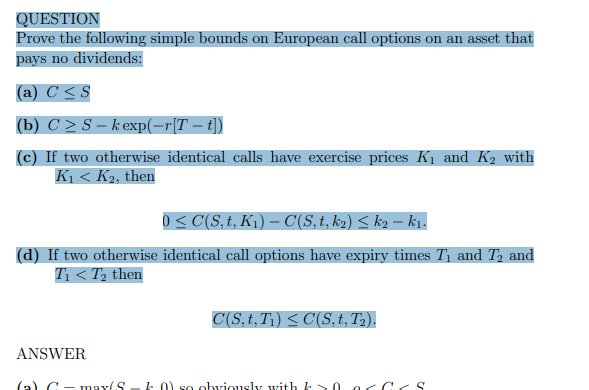

TD - Simple bounds on European call options

RM 20.29

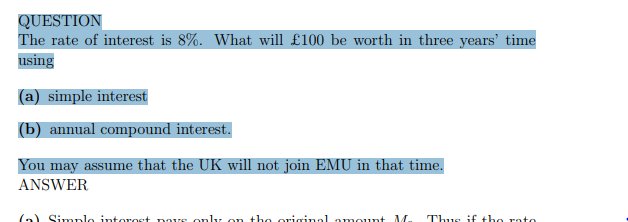

TD - Simple and annual compound interest

RM 20.29

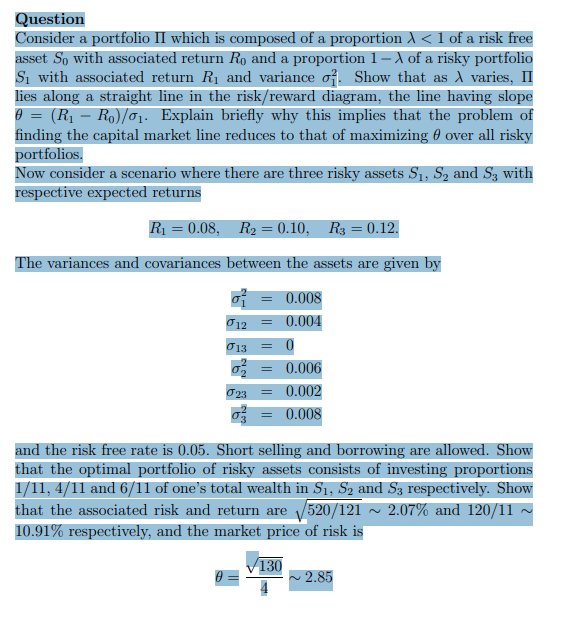

TD - Riskless and risky investments and the market price of risk

RM 40.57

TD - Risk free and risky assets and the market price of risk-Quiz & sol

RM 40.57

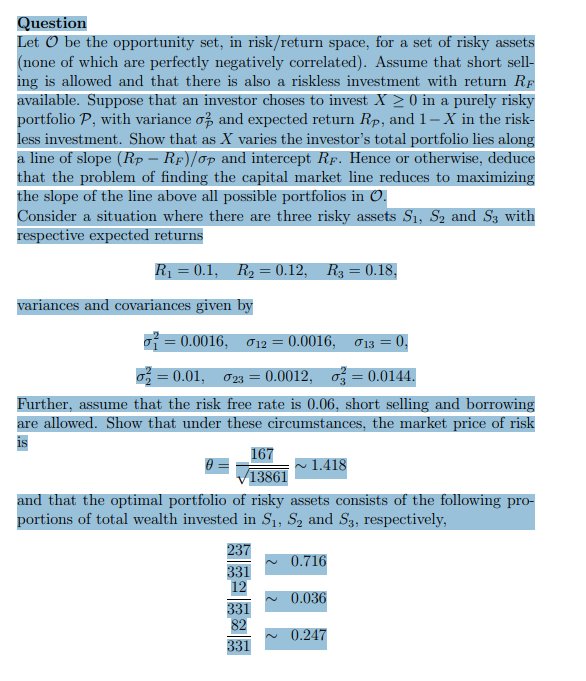

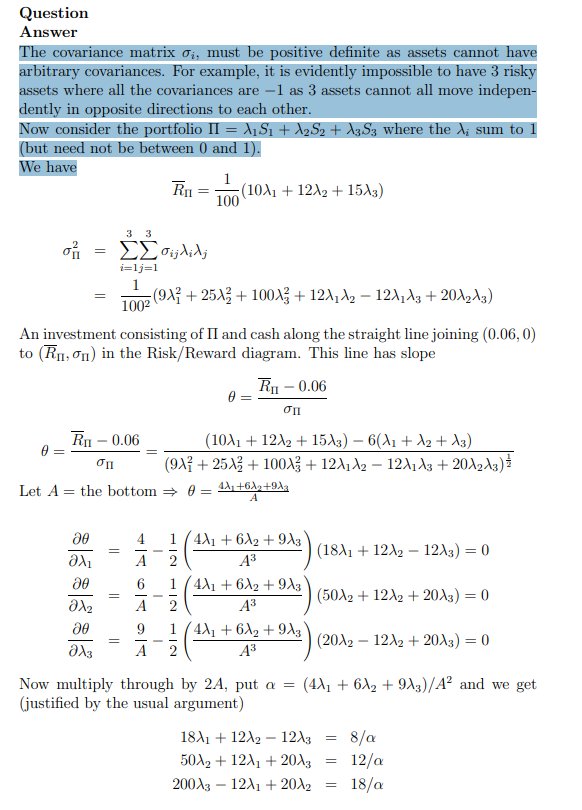

TD - Real world assets, the covariance matrix and the market price of risk

RM 12.17

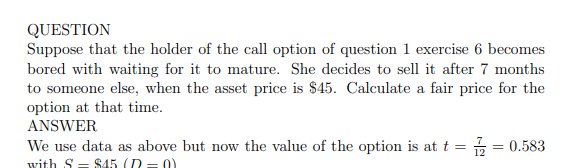

TD - Profit or loss on options and the Black-Scholes equation

RM 40.57

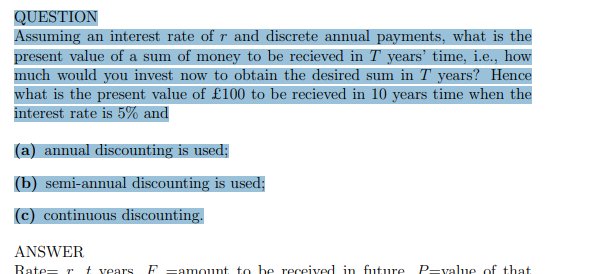

TD - Present value using annual, semi-annual or continuous discounting

RM 40.57

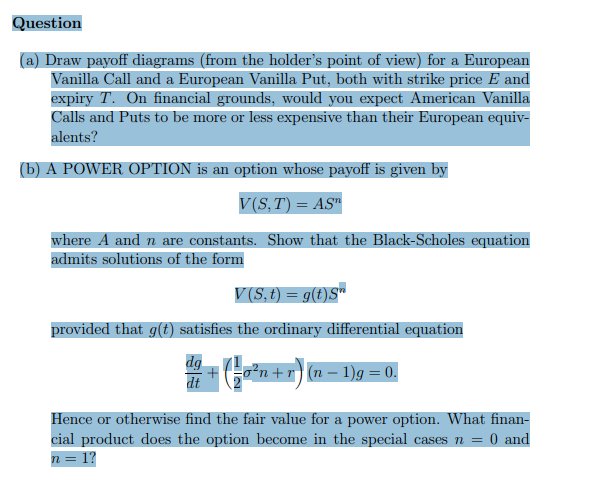

TD - Payoff diagrams, a power option and the Black-Scholes equation

RM 40.57

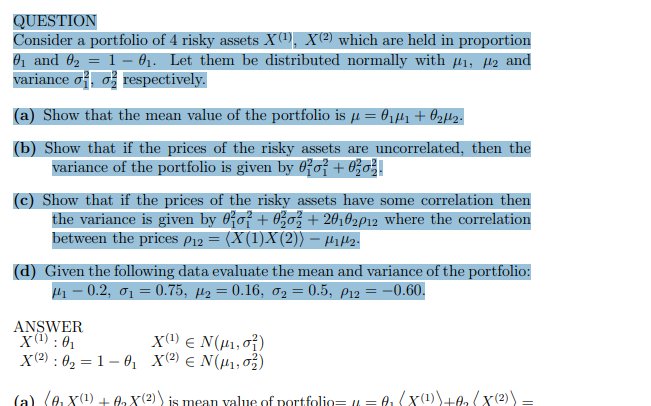

TD - Normally distributed risky assets and their mean and variances

RM 40.57

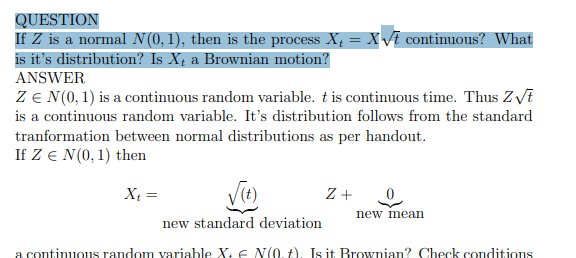

TD - Normal distribution and Brownian motion

RM 20.29

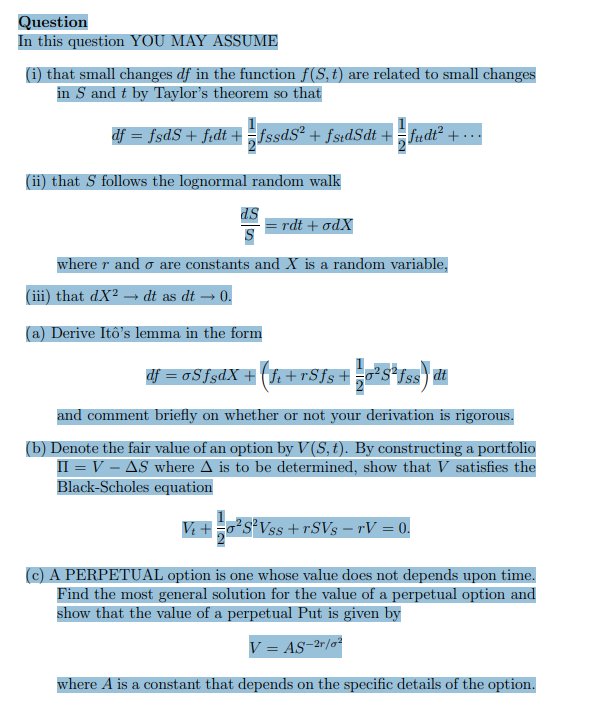

TD - Itos lemma, Black-Scholes equation and a perpetual option

RM 40.57

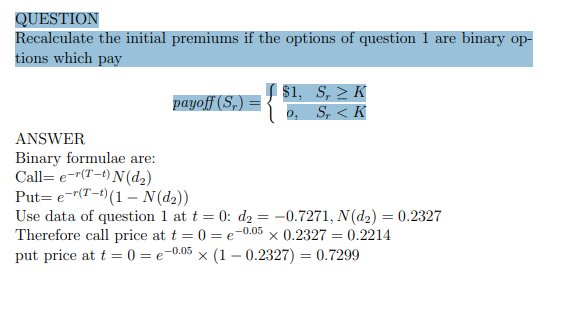

TD - Initial premiums for binary options

RM 20.29

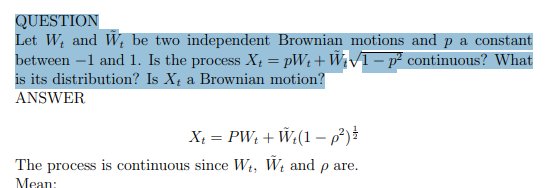

TD - Independent Brownian motions-Quiz & Sol

RM 40.57

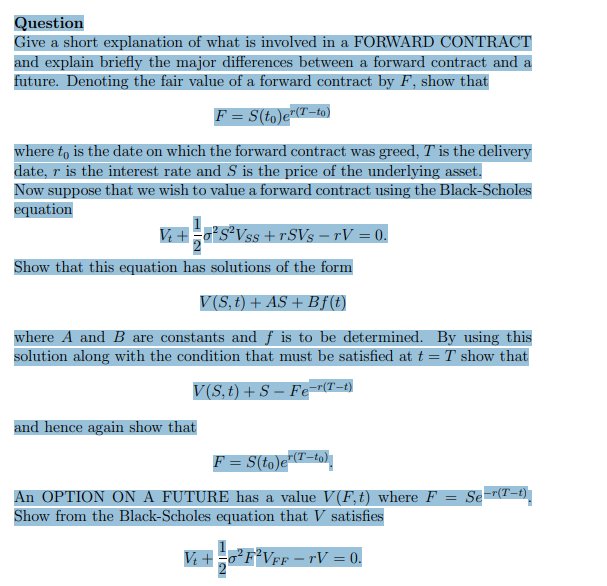

TD - Forward contract, Black-Scholes equation and an option on a future

RM 40.57

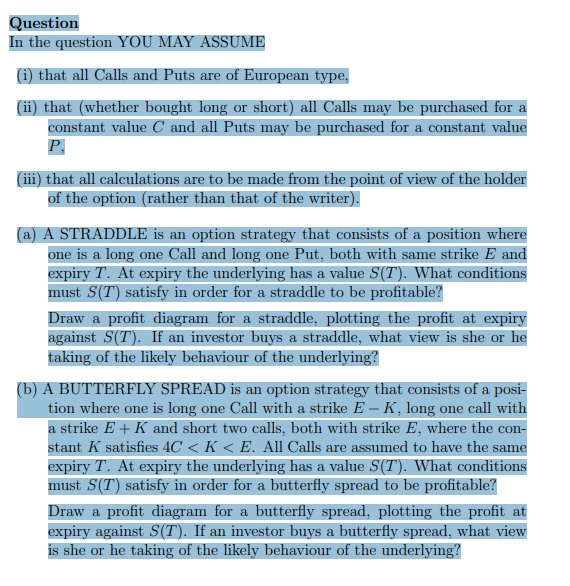

TD - European calls and puts, a straddle and a butterfly spread

RM 40.57

TD - European call options- quiz & solution

RM 40.57

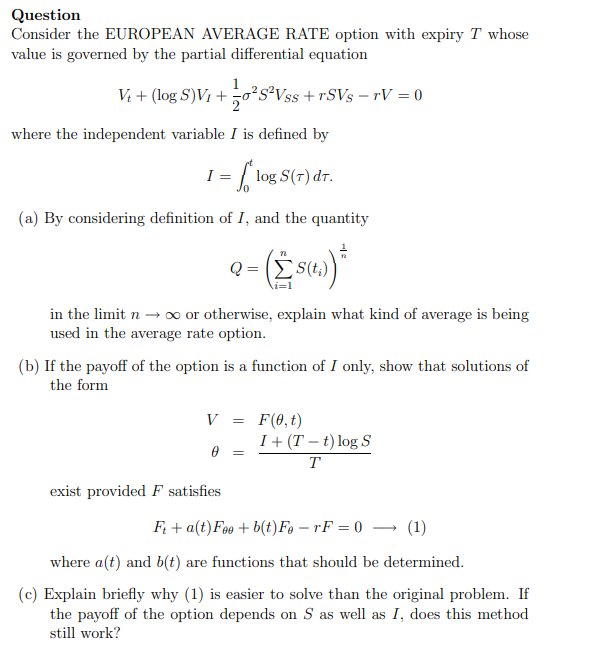

TD - European average rate option- Quiz & Solution

RM 40.57

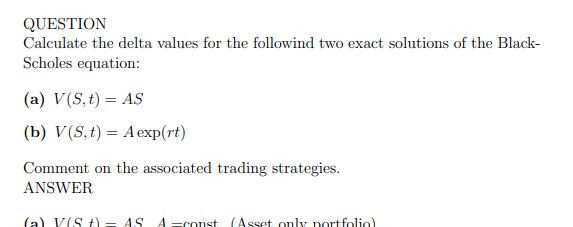

TD - Delta values for exact solutions of the Black-Scholes equation

RM 40.57

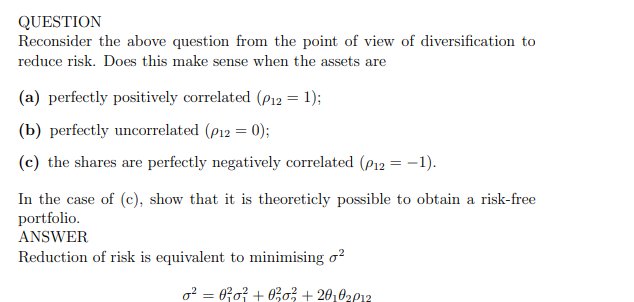

TD - Correlated and uncorrelated assets

RM 40.57

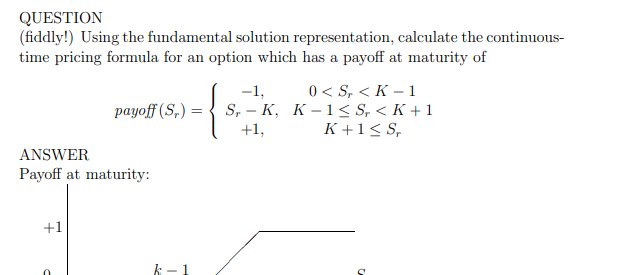

TD - Continuous time pricing formula for an option

RM 40.57

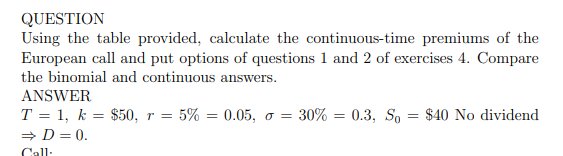

TD - Continuous time premiums of European call and put options

RM 40.57

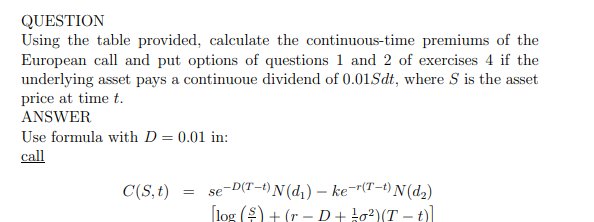

TD - Continuous dividend and European call and put options

RM 40.57

TD - Constant interest rates- quiz and solution

RM 20.29

TD - Compound interest- quiz-solution

RM 40.57

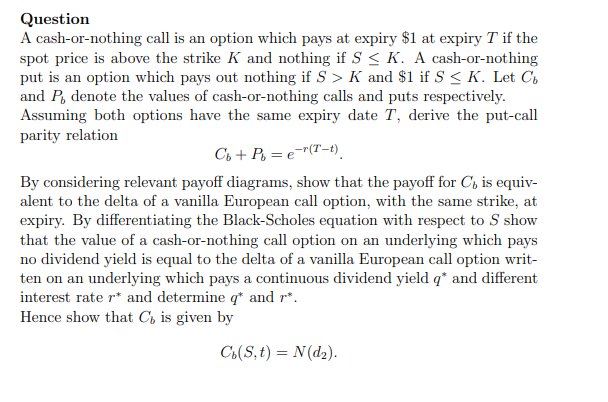

TD - Cash-or-nothing puts and calls, payoff diagrams and the Black-Scholes equation-Solution

RM 40.57

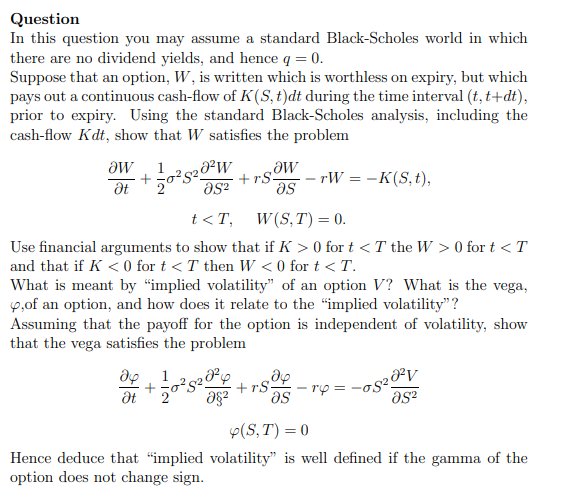

TD - Black-Scholes, implied volatility and payoff

RM 40.57

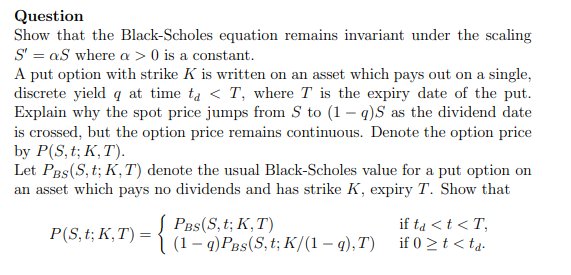

TD - Black-Scholes equation, spot price and option price

RM 40.57

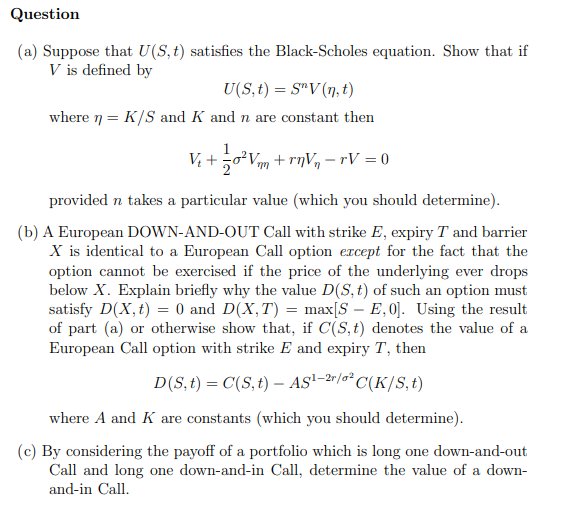

TD - Black-Scholes equation, a European down-and-out call and the payoff of a portfolio

RM 40.57

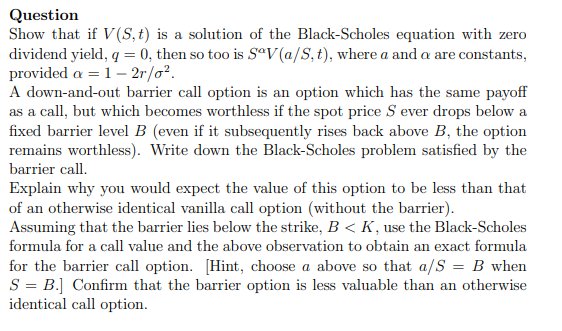

TD - Black-Scholes equation and a down-and-out barrier call option

RM 40.57

TD - Black-Scholes and call options

RM 40.57

TD - Black-Scholes and a European forward-start call option

RM 40.57

TD - Binomial model for asset price changes

RM 40.57

TD - Assets prices and European call options

RM 40.57

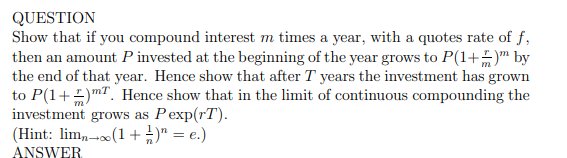

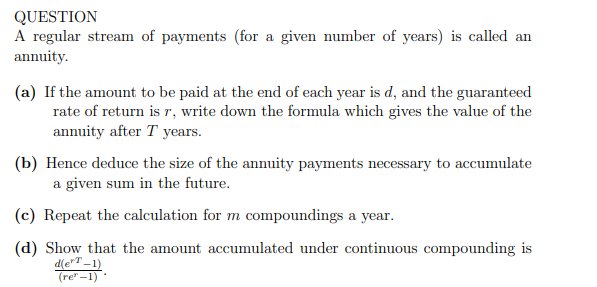

TD - Annuity and continuous compounding

RM 40.57

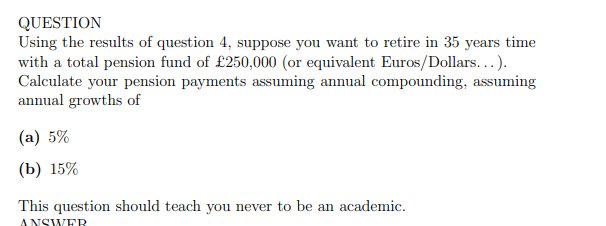

TD - Annual compounding with various annual growths

RM 40.57

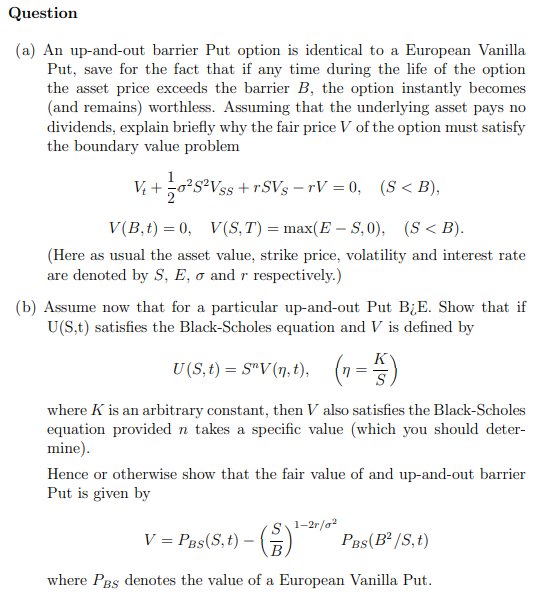

TD - An up-and-out barrier put option and the Black-Scholes equation

RM 40.57

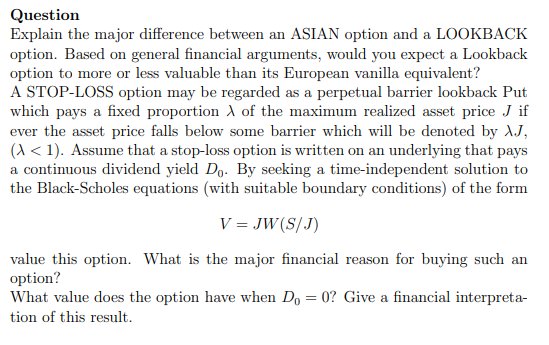

TD - An Asian option, a lookback option and a stop-loss option

RM 40.57

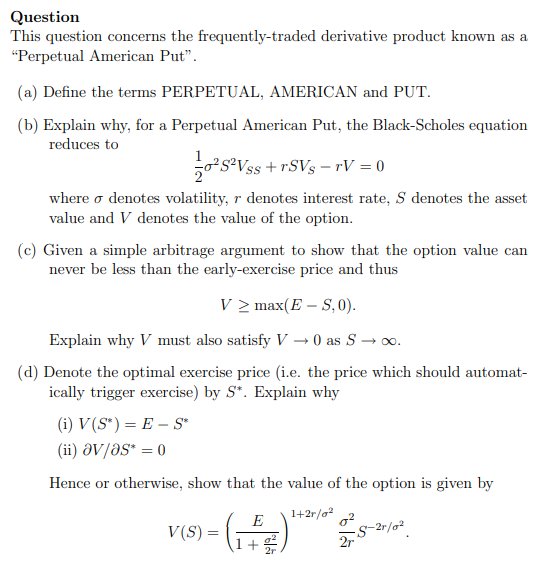

A perpetual American put, the Black-Scholes equation and the optimal exercise price

RM 40.57

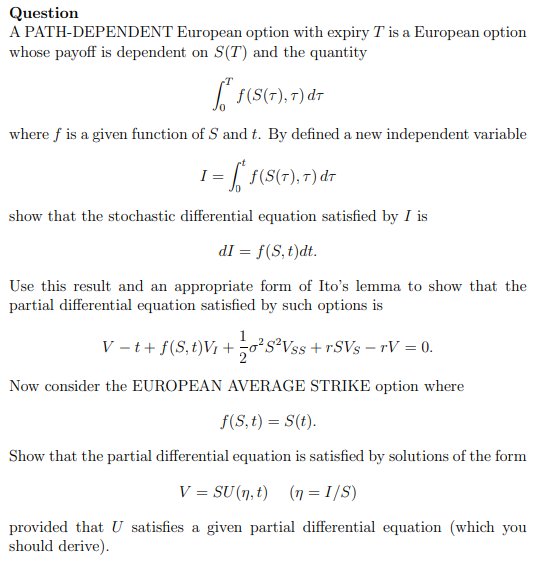

A path-dependent European option and the European strike average

RM 40.57

TD - a European vanilla call, the delta of an option and the portfolio

RM 28.40

Chevron Left

1

2

3

4

Chevron Right

View as:

Admin

Supporter

Edit collection

Go to dashboard

View as

Admin

Supporter

Go to dashboard