TD - Black-Scholes equation, a European down-and-out call and the payoff of a portfolio

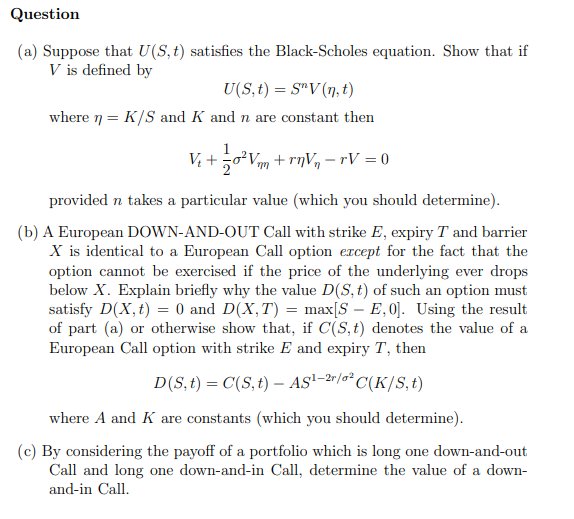

Question

(a) Suppose that U(S,t) satisfies the Black-Scholes equation. Show that if

V is defined by

U(S,t) = S

nV (η,t)

where η = K/S and K and n are constant then

Vt +

1

2

σ

2Vηη + rηVη − rV = 0

provided n takes a particular value (which you should determine).

(b) A European DOWN-AND-OUT Call with strike E, expiry T and barrier

X is identical to a European Call option except for the fact that the

option cannot be exercised if the price of the underlying ever drops

below X. Explain briefly why the value D(S,t) of such an option must

satisfy D(X,t) = 0 and D(X, T) = max[S − E, 0]. Using the result

of part (a) or otherwise show that, if C(S,t) denotes the value of a

European Call option with strike E and expiry T, then

D(S,t) = C(S,t) − AS1−2r/σ2

C(K/S,t)

where A and K are constants (which you should determine).

(c) By considering the payoff of a portfolio which is long one down-and-out

Call and long one down-and-in Call, determine the value of a downand-in Call.