TD - An up-and-out barrier put option and the Black-Scholes equation

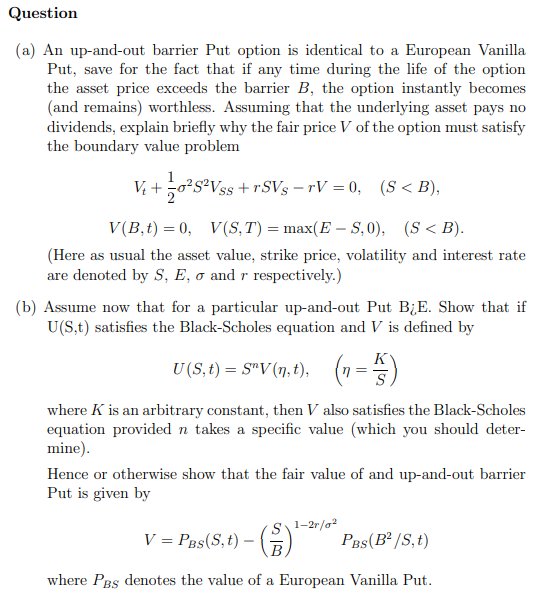

Question

(a) An up-and-out barrier Put option is identical to a European Vanilla

Put, save for the fact that if any time during the life of the option

the asset price exceeds the barrier B, the option instantly becomes

(and remains) worthless. Assuming that the underlying asset pays no

dividends, explain briefly why the fair price V of the option must satisfy

the boundary value problem

Vt +

1

2

σ

2S

2VSS + rSVS − rV = 0, (S < B),

V (B,t) = 0, V (S, T) = max(E − S, 0), (S < B).

(Here as usual the asset value, strike price, volatility and interest rate

are denoted by S, E, σ and r respectively.)

(b) Assume now that for a particular up-and-out Put B¿E. Show that if

U(S,t) satisfies the Black-Scholes equation and V is defined by

U(S,t) = S

nV (η,t),

µ

η =

K

S

¶

where K is an arbitrary constant, then V also satisfies the Black-Scholes

equation provided n takes a specific value (which you should determine).

Hence or otherwise show that the fair value of and up-and-out barrier

Put is given by

V = PBS(S,t) −

µ

S

B

¶1−2r/σ2

PBS(B

2

/S,t)

where PBS denotes the value of a European Vanilla Put.