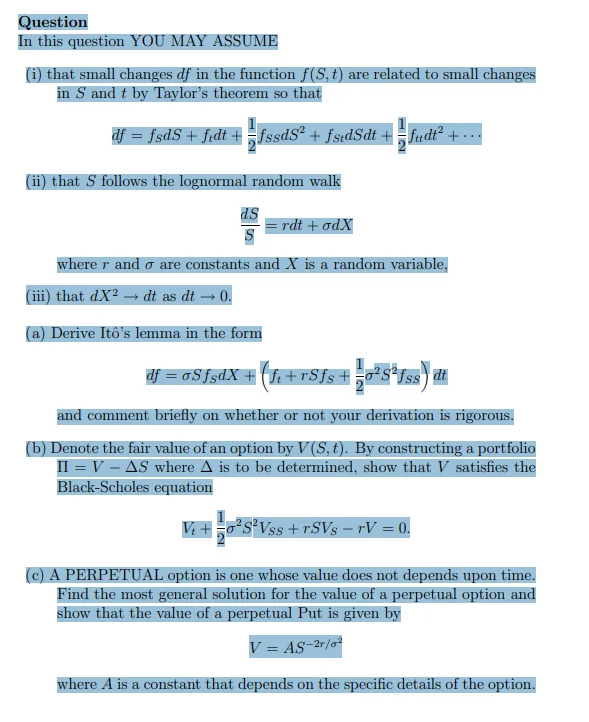

TD - Itos lemma, Black-Scholes equation and a perpetual option

Question

In this question YOU MAY ASSUME

(i) that small changes df in the function f(S,t) are related to small changes

in S and t by Taylor’s theorem so that

df = fSdS + ftdt +

1

2

fSSdS2 + fStdSdt +

1

2

fttdt2 + · · ·

(ii) that S follows the lognormal random walk

dS

S

= rdt + σdX

where r and σ are constants and X is a random variable,

(iii) that dX2 → dt as dt → 0.

(a) Derive Itˆo’s lemma in the form

df = σSfSdX +

µ

ft + rSfS +

1

2

σ

2S

2

fSS

¶

dt

and comment briefly on whether or not your derivation is rigorous.

(b) Denote the fair value of an option by V (S,t). By constructing a portfolio

Π = V − ∆S where ∆ is to be determined, show that V satisfies the

Black-Scholes equation

Vt +

1

2

σ

2S

2VSS + rSVS − rV = 0.

(c) A PERPETUAL option is one whose value does not depends upon time.

Find the most general solution for the value of a perpetual option and

show that the value of a perpetual Put is given by

V = AS−2r/σ2

where A is a constant that depends on the specific details of the option.