TD - Correlated and uncorrelated assets

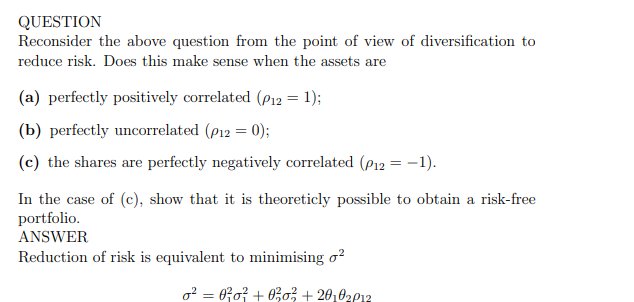

QUESTION

Reconsider the above question from the point of view of diversification to

reduce risk. Does this make sense when the assets are

(a) perfectly positively correlated (ρ12 = 1);

(b) perfectly uncorrelated (ρ12 = 0);

(c) the shares are perfectly negatively correlated (ρ12 = −1).

In the case of (c), show that it is theoreticly possible to obtain a risk-free

portfolio.