TD - Black-Scholes, implied volatility and payoff

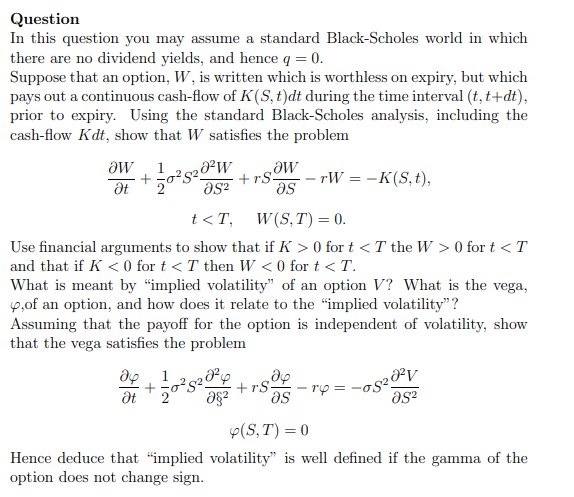

Question

In this question you may assume a standard Black-Scholes world in which

there are no dividend yields, and hence q = 0.

Suppose that an option, W, is written which is worthless on expiry, but which

pays out a continuous cash-flow of K(S,t)dt during the time interval (t,t+dt),

prior to expiry. Using the standard Black-Scholes analysis, including the

cash-flow Kdt, show that W satisfies the problem

∂W

∂t

+

1

2

σ

2S

2

∂

2W

∂S2

+ rS

∂W

∂S

− rW = −K(S,t),

t < T, W(S, T) = 0.

Use financial arguments to show that if K > 0 for t < T the W > 0 for t < T

and that if K < 0 for t < T then W < 0 for t < T.

What is meant by “implied volatility” of an option V ? What is the vega,

ϕ,of an option, and how does it relate to the “implied volatility”?

Assuming that the payoff for the option is independent of volatility, show

that the vega satisfies the problem

∂ϕ

∂t

+

1

2

σ

2S

2

∂

2ϕ

∂§

2

+ rS

∂ϕ

∂S

− rϕ = −σS

2

∂

2V

∂S2

ϕ(S, T) = 0

Hence deduce that “implied volatility” is well defined if the gamma of the

option does not change sign.