TD - Assets prices and European call options

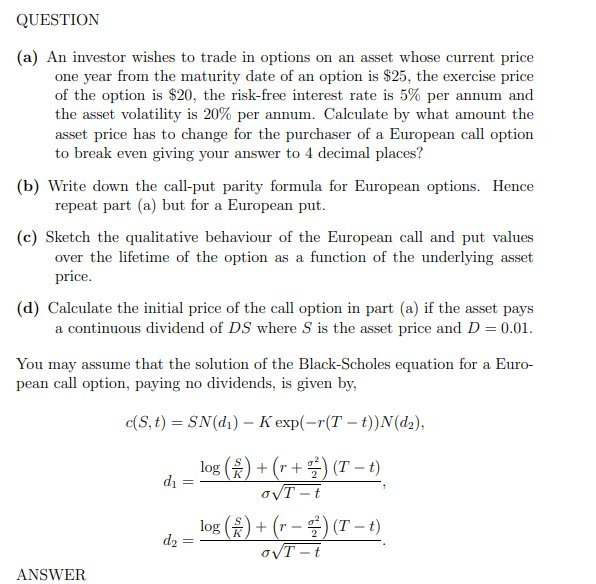

QUESTION

(a) An investor wishes to trade in options on an asset whose current price

one year from the maturity date of an option is $25, the exercise price

of the option is $20, the risk-free interest rate is 5% per annum and

the asset volatility is 20% per annum. Calculate by what amount the

asset price has to change for the purchaser of a European call option

to break even giving your answer to 4 decimal places?

(b) Write down the call-put parity formula for European options. Hence

repeat part (a) but for a European put.

(c) Sketch the qualitative behaviour of the European call and put values

over the lifetime of the option as a function of the underlying asset

price.

(d) Calculate the initial price of the call option in part (a) if the asset pays

a continuous dividend of DS where S is the asset price and D = 0.01.

You may assume that the solution of the Black-Scholes equation for a European call option, paying no dividends, is given by,

c(S,t) = SN(d1) − K exp(−r(T − t))N(d2),

d1 =

log ³

S

K

´

+

³

r +

σ

2

2

´

(T − t)

σ

√

T − t

,

d2 =

log ³

S

K

´

+

³

r −

σ

2

2

´

(T − t)

σ

√

T − t